The Accounting Game

Darrell Mullis and Judith Orloff

GENRE: Business & Finance

GENRE: Business & Finance

PAGES: 220

PAGES: 220

COMPLETED: October 26, 2021

COMPLETED: October 26, 2021

RATING:

RATING:

Short Summary

Darrell Mullis and Judith Orloff break down difficult financial statements by taking readers through the day-to-day, minute-by-minute operations of a kid’s lemonade stand. Using the stand as an example, the authors show how certain transactions and financial events affect the income statement and balance sheet in different ways. The book is fun, easy to understand, and will quench the thirst of anyone looking to learn about financial statements!

Key Takeaways

Financial Ratios are Key — Most accounting numbers don’t mean much by themselves. When you use the numbers in financial statements to create ratios, the numbers begin to have actual meaning and you can compare the ratios to competitors in the industry. Ratios ultimately reveal a company’s financial health, and you can use them to gauge the company’s year-over-year performance.

Financial Ratios are Key — Most accounting numbers don’t mean much by themselves. When you use the numbers in financial statements to create ratios, the numbers begin to have actual meaning and you can compare the ratios to competitors in the industry. Ratios ultimately reveal a company’s financial health, and you can use them to gauge the company’s year-over-year performance.

Straight Cash, Homie — Ultimately, cash is king. A company can survive despite not turning in a profit, but the business is done if it runs out of money. Cash is the lifeblood of the business. High cash and low debt is what you’re looking for.

Straight Cash, Homie — Ultimately, cash is king. A company can survive despite not turning in a profit, but the business is done if it runs out of money. Cash is the lifeblood of the business. High cash and low debt is what you’re looking for.

The Balance Sheet Will Always Balance — The formula for the balance sheet is Assets – Liabilities = Shareholder Equity. Because Shareholder Equity is owed to shareholders, it can be thought of, for balance sheet purposes, as a liability. Therefore, it’s always going to balance out.

The Balance Sheet Will Always Balance — The formula for the balance sheet is Assets – Liabilities = Shareholder Equity. Because Shareholder Equity is owed to shareholders, it can be thought of, for balance sheet purposes, as a liability. Therefore, it’s always going to balance out.

Favorite Quote

"On a daily basis, cash runs the business NOT profits."

Book Notes

*Did not take chapter-by-chapter notes on this one. Running list below.

- Quote: “On a daily basis, cash runs the business NOT profits.”

- Earnings are not cash!

- Earnings + the original investment just show you what portion of your total assets are yours

- Cash is the driving force and the blood of the business. Cash is king.

- You can run a business without profits for awhile. You CANNOT run a business without cash!

- Balance Sheet

- The Balance Sheet is always going to balance

- Assets = Liabilities + Shareholder Equity

- The way to think about this: Shareholders Equity is technically a liability

- Accounts Payable is money you owe back in the short term for borrowed supplies and goods.

- What we owe Papy the grocery store manager.

- Notes Payable is money you owe back (usually to the bank) over the long term for money borrowed

- Notes payable is borrowed money (DEBT) and debt always comes with interest payments. Accounts payable does not have interest, normally.

- Interest expenses show up on the income statement because it’s an EXPENSE and a cost of doing business.

- When you see notes payable on the balance sheet, this represents the principle of the debt, not the principle AND the interest.

- Retained Earnings is money that accumulates and piles up over the years.

- It can be used to pay dividends to shareholders or grow/expand the business

- Accounts Receivable is an asset.

- What your buddies who bought lemonade from you still owe you because you let them buy on credit.

- Specifically, it’s a current asset. It’s what is owed to you in cash in the short term because you allowed the other person or company to buy your product on credit.

- Prepaid Expenses are an asset on the balance sheet. They are paid for in advance and you receive them over time.

- Ex. Insurance coverage

- I like the example of a Sports Illustrated magazine subscription. You pay for the subscription at the beginning of the year and you receive a new Sports Illustrated magazine to read every month. This is an asset.

- You would think a Prepaid Expense would be an expense or a liability, but Prepaid Expenses are an asset because you’re paying for something that has value into the future.

- Think of it like this: If you paid $3 ahead of time for a 3-year insurance coverage policy and decided to get rid of it after the first year, you would receive $2 back from the insurance company. Therefore, Prepaid Expenses are considered an asset.

- Inventory

- When studying a company’s inventory on the balance sheet, look at the previous year’s inventory to determine what the inventory started at for the current year you are analyzing.

- The balance sheet for a company on a 10-K report is a snapshot of the company’s financial condition for the final day of the business year. So what is listed in inventory in the previous year’s balance sheet will be the inventory that the current year started out at.

- Ex. Analyzing 2020 year-end inventory for a company. Look at 2019’s balance sheet to see what inventory started at in the beginning of 2020.

- FIFO and LIFO were created because of the differences in price companies pay over time for raw materials.

- Ex. We bought lemons for 20 cents per pound in Week 1 of the lemonade stand but the price went up to 40 cents per pound by Week 3

- FIFO

- Net income will be higher because COGS will be lower. Company will appear more profitable compared to LIFO.

- The first items of inventory in are the first out when making the product.

- Pipeline Analogy: Picture a pipe that has two ends. Picture putting the first lemons into the pipeline first. They will be the first to come out the other side

- With FIFO, if the first raw materials are cheaper than later raw materials, COGS is always going to be lower and therefore net income will be higher because you are using cheaper raw materials to make the product. Also, ending inventory will be higher because the more expensive raw materials are still sitting there in inventory.

- LIFO

- Net income will appear lower, which means lower taxes owed. This is the ONLY REASON a company would choose LIFO inventory method.

- The last items of inventory in are the first out when making the product.

- Barrel Analogy: Picture a barrel. Picture filling the barrel with the lemons. The last ones thrown in the barrel will be the first out.

- With LIFO, if the later raw materials in the barrel are more expensive than the first raw materials in the barrel, COGS is always going to be higher and therefore net income will be lower because you are using more expensive raw materials to make the product, which cuts into the bottom line. Inventory will also be lower because the cheaper raw materials are sitting in inventory still.

- A note on FIFO and LIFO:

- The bottom line net income differences largely depend on prices for raw materials in the market. In our lemons example, prices for lemons were rising, therefore FIFO will result in higher net income and lower COGS. However, if prices for lemons were falling, FIFO would result in lower net income and higher COGS because you’re using the “first in” raw materials that were priced higher at the time.

- The choice between FIFO and LIFO comes down to your tax strategy (do you want to pay lower taxes?) and the price direction for raw materials in your industry (are prices going up or down?)

- Companies tell you which method they are using in the footnotes.

- Most companies use FIFO. LIFO records are difficult and expensive to maintain.

- The Balance Sheet is always going to balance

- Cash Flow Statement

- Records only the cash that comes in and out in a given time period

- Transactions or events made on credit will not impact this statement at all. Only cash expenditures or inflows.

- This is more of a supplement to the balance sheet and income statement. Ending Cash will match what is listed in the balance sheet, BUT the cash flow statement will actually tell you exactly where your cash went and how much came in and how much came out over a period of time.

- Records only the cash that comes in and out in a given time period

- Accrual Method of Accounting:

- Also called the “Not-Only-Cash Method”

- Accounting for every transaction as it happens regardless of whether or not cash has been paid at the time

- Became a method when people stopped paying cash for everything. People were beginning to use credit and cash was changing hands at a later date.

- The Accrual Method acts like cash changed hands at the time for every transaction, even if it was using credit.

- Essentially, sales are recognized AT THE TIME OF THE TRANSACTION NOT WHEN CASH IS ACTUALLY RECEIVED

- Another way to think about it: The Accrual Method pretends that cash was used and exchanged on every sale or transaction.

- Accrual Method is more accurate than the Cash Method because it accounts for everything, not just cash events.

- Cash Method of Accounting:

- Only accounts for things ONLY when they happen in CASH

- Transactions or earnings on credit ARE NOT accounted for.

- Therefore, less accurate.

- Best for tax purposes because you will always show less profit when only accounting for cash events.

- If a company has inventory on its balance sheet, it MUST use the Accrual Method.

- Service companies with no inventory can use the cash method.

- Interestingly, service companies can report to the IRS using the Cash Method (which will always show lower profits for less taxes) but report to investors using the Accrual Method (which will always show higher profit because it’s more accurate and accounts for all events).

- This is called “creative accounting”

- Only accounts for things ONLY when they happen in CASH

- Capitalizing — Buying Fixed Assets goes on the Balance Sheet, not the Income Statement

- This is because you are “capitalizing the asset” because it’s an improvement not expensing it (which would go on the income statement)

- Capitalizing on the balance sheet is done with long term assets that will last awhile and are improvements

- Fixed Assets = Plant, Property, Equipment

- Ex. Lemonade stand paint. If it was the super duper paint, it would last 10 years and you would capitalize it under fixed assets on the balance sheet. We used the cheap stuff, which wears away after a year so you have to continuously put new paint on. This is an “ongoing cost of business” and would be expensed on the income statement and therefore reduces earnings.

- Ex. Lemonade stand sink. It’s an improvement that will last many years, therefore we will capitalize it on the balance sheet under fixed assets rather than expense it as an “ongoing cost of doing business” on the income statement.

- There are two main criteria that decides whether an item is capitalized or expensed:

- How long does the item last? You capitalize something that lasts over a year. You expense items that last under a year.

- If you buy a trash can and it lasts longer than a year, would it be capitalized? No. It’s too insignificant of an item.

- Straight Line Depreciation

- Allows you to depreciate the value of your asset over time

- Only available for buildings, not equipment

- Each year, you depreciate the asset an equal amount. This amount is determined by taking the cost of the asset and the number of years it will last. See image.

- The value of your asset is going down ON PAPER (book value). It may be going up in real life though.

- To account for depreciation, the value of the fixed asset decreases on the balance sheet. It’s regarded as an expense on the income statement and therefore lowers earnings.

- On the income statement, it’s listed as “Depreciation Expense”

- Key Rule: Depreciation is a non-cash expense

- This is key because companies are able to reduce their earnings (and therefore pay less taxes) by having depreciation expense. And when they do this, cash is NOT being reduced in the process.

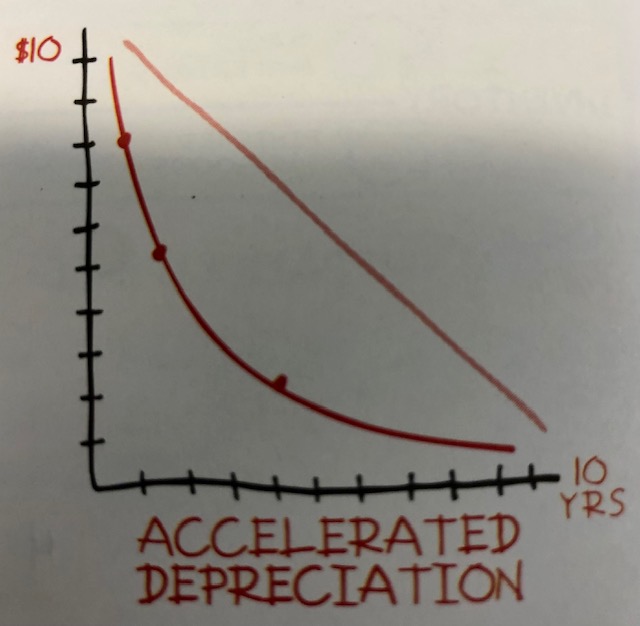

- Accelerated Depreciation

- Allows you to depreciate the value of your asset over time at an accelerated rate

- Only can be used on equipment, not buildings

- This method of depreciation allows you to take a greater amount of the asset’s depreciation in the earlier years and less in the later years

- This is good for lowering earnings (because annual depreciation expense is an expense on the income statement) which results in reporting less net income and therefore paying less in taxes.

- It’s the government’s way of encouraging businesses to buy and sell assets, which stimulates the economy

- Allows you to depreciate the value of your asset over time at an accelerated rate

- More Balance Sheet Notes

- Gross Fixed Assets = Total purchase price of ALL fixed assets

- Equipment and buildings

- Accumulated Depreciation = Total depreciation taken to date on ALL assets

- If “accumulated depreciation” is low compared to “gross fixed assets”, it shows that the company’s assets are fairly new

- Net Fixed Assets = Gross Fixed Assets – Accumulated Depreciation

- Also called “net book value”

- Gross Fixed Assets = Total purchase price of ALL fixed assets

- Financial Ratios

- These allow us to better gauge the performance of the business by giving us good numbers to use to compare year-to-year performance and to industry competitors

- Look over several years to identify trends

- The analogy of looking at the Chicago Bulls over several seasons instead of one game is a good one.

- On the income statement, it’s good to divide key line items into sales to get good ratios

- Ex. $250 in sales and $115 in COGS. Divide $115 into $250 = 0.46.

- Interpretation: For every $100 in sales, we spent $46 on COGS to produce the product.

- You can do this with every line item and compare to past performance and to competition

- COGS, Operating Expenses, and Net Profit are the three major line items you should use as we just did in the above example to create ratios.